.jpg)

For financial service companies, reputation is of paramount importance. If public trust in a brand takes a hit, old customers flee and new ones stay clear. Consistent compliance with regulations that govern consumer interactions is therefore critical not only for staying on the right side of the law and avoiding penalties and fines, but also for establishing and maintaining a sterling reputation as an honest, upstanding, law-abiding and consumer-oriented organization.

Compliance, however, is not trivial to achieve -- or to maintain. The regulatory landscape is a complex patchwork of local, national and regional laws, policies and regulations. Financial service providers that operate internationally or across state borders must be aware of them all and ensure that each interaction complies with those that are relevant. Despite best intentions, it’s easy to err.

To enable ongoing compliance monitoring as well as audits, each interaction with each customer or prospect -- via phone, email, chat, social media or any other channel or medium -- must be carefully documented and filed away for easy access. Once recorded, customer interaction data is archived and undergoes a process of reconciliation, management, and enrichment. The data is analyzed and interactions assessed for compliance.

The Only Constant is Change

A quality monitoring process that was once limited to tracking phone conversations has now been broadened to cover touchpoints including websites, email, SMS, Skype/VoIP, chats and instant messaging. Interactions from diverse media must be recorded and archived. In too many organizations, however, as communication channels have been added, channel-specific recording solutions have been added as well. The result is silos of isolated data for each channel. As a result, tracking each customer’s conversational journey across multiple channels is difficult at best, if possible at all.

With multi-channel communications increasingly the norm, consolidated recording and monitoring solutions are essential. To manage compliance, financial service organizations must be able to track, monitor and analyze communications, regardless of how they occur, and follow the customer journey from first contact through to completion. They need flexible, scalable solutions that can efficiently manage the large quantities of diverse data that they are collecting.

Changing communications technologies are not the only reason -- or even the primary reason -- why flexibility is essential for customer interaction management solutions. Most financial service organizations operate across multiple jurisdictions and state, national and international borders. Regulations are constantly being updated and changed, and managing those changes -- ensuring that they are promptly and properly recorded and implemented in the system -- is no trivial task.Each change may impact multiple functions within the organization. Ensuring uninterrupted compliance across locations as requirements change is no simple task.

Automation is the Only Answer

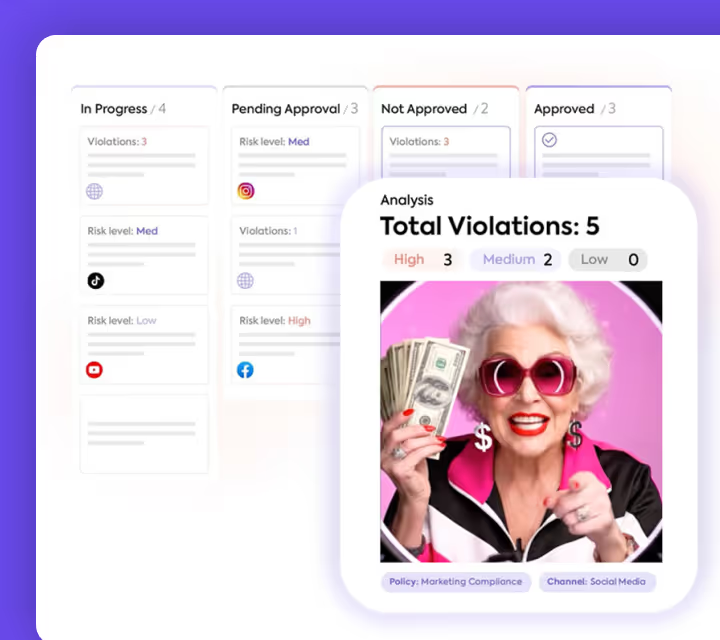

Today, it’s no longer feasible to depend on slow and imprecise manual updating processes when regulations change. Agile businesses need all regulatory systems to be “go” when entering new regions, or when regulations are updated. Likewise, manual quality checks of random interactions no longer suffice since they present only a single slice of what is often a multi-channel interaction . For auditing purposes, journey-level recording, archiving, and monitoring is essential.

Digital transformation initiatives have already revolutionized numerous business processes, reducing operational complexity and costs. Regulatory compliance is now on the cusp of a similar change. A new generation of reg-tech solutions is easing the regulatory compliance burden with flexible, scalable automated solutions for recording, archiving, monitoring and analyzing not just customer interactions, but full conversational journeys.

Sedric transforms monitoring from a burden required by regulatory bodies into a positive agent of change. With all interactions rapidly scanned, compliance officers can quickly and accurately identify and examine those that are problematic, and identify precisely how compliant the company is. Using AI, it enables organizations to leverage their vastf interaction data, extracting actionable information and applying it to enhance the user experience and build brand value, as well as improving compliance.

Discover how Sedric can help your organization streamline QA, improve the customer experience and enhance your brand equity.