.jpg)

In the fast-paced and heavily regulated world of financial services, compliance officers serve as the gatekeepers. The burden of navigating a labyrinth of regulations that can shift overnight falls squarely on their shoulders, and there’s little room for errors or mishaps.

The weight of this responsibility is enormous and it’s no surprise that many compliance officers find themselves grappling with the stress of the job long after they’ve left their office or shut their laptop for the day. So, what keeps a compliance manager up late at night? Here are some of the top concerns, based on both industry trends and my own experiences working closely with compliance professionals.

1. Frequent Regulatory Changes

As someone deeply immersed in the compliance space in the last 3 years (with zero experience before that), I’ve seen firsthand how constant updates to regulations can overwhelm even the most seasoned compliance officers. Whether it’s MiFID II in the EU, which continues to evolve and expand, the new Consumer Duty regulations in the UK aimed at ensuring fair treatment of customers, or FINRA’s constant adjustments, staying ahead of these changes is critical, but confusing. Requirements change constantly, adherence is expected, and penalties can be steep.

Trying to do it manually is virtually impossible, especially for global businesses who operate in many jurisdictions and languages, or for companies with large partner programs. The stakes are high, and new regulations can quickly go into effect without much warning.

Compliance teams need rock-solid strategies for ensuring they are on top of regulatory changes in every jurisdiction where they operate. They also need to be agile and active, able to quickly adapt to any changes. This requires good team communication and strong relationships with marketing and product teams. Any glitch in these systems of regulatory monitoring and internal comms can quickly put the company at risk.

2. Data Privacy and Cybersecurity Threats

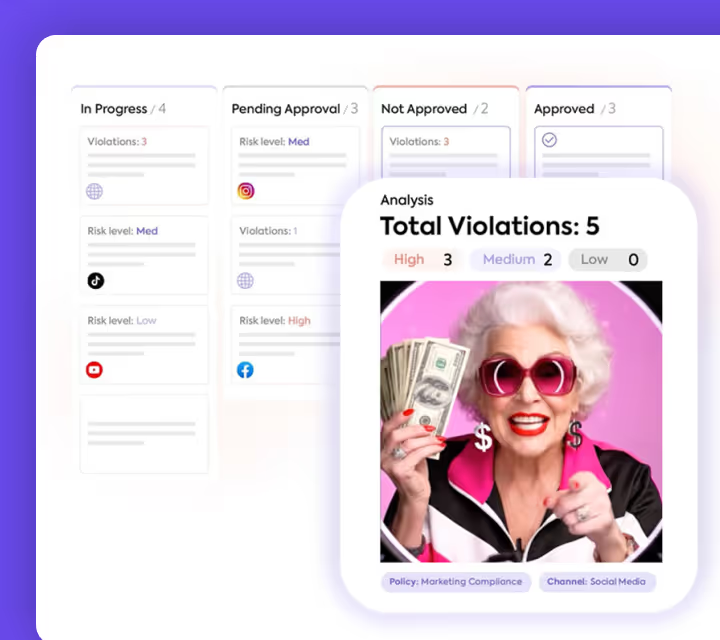

With cyber threats growing more sophisticated by the day, data privacy is no longer just a regulatory requirement - it's a cornerstone of consumer trust. In my discussions with industry professionals, it’s clear that the fear of a data breach, especially under the strict guidelines of GDPR and CCPA, is a top concern. Companies that leverage AI to continuously monitor and respond to threats are better positioned to protect their data and stay compliant with these complex regulations. A proactive, technology-driven approach is becoming a best practice across the industry, if not a necessity.

3. AML and KYC Challenges

Anti-Money Laundry (AML) and Know Your Customer (KYC) regulations play crucial roles in preventing financial crimes, but they also present a significant challenge due to the sheer volume of transactions that need to be monitored. As one compliance officer described this to me last week, “It really is looking for a needle in a haystack,” especially for companies that must adhere to both FINRA’s stringent AML requirements in the US as well as MiFID II’s transparency rules in the EU. AI tools are a game changer in this realm; they can sift through vast amounts of data to detect anomalies reducing the manual burden and increasing accuracy.

4. Third-Party Risk Management

Managing third-party risks is another area where compliance officers can feel overwhelmed. With global operations becoming more complex and regulatory bodies paying closer attention, the need to ensure that every partner and vendor complies with regulations and company guidelines can be daunting. Automating due diligence processes saves time while also significantly reducing the risk of oversights. This is especially true when dealing with vendors in multiple jurisdictions, where regulations can vary widely. As every compliance team knows, their company can and will be held liable for the transgressions of their affiliates, making it imperative to have a good system for monitoring risk.

5. Personal Liability

Personal liability is a relatively new concern plaguing the most vigilant compliance officers, especially with the CFPB's recent enforcement actions highlighting individual accountability. At a conference last summer, a fintech client shared with me his own anxiety about facing personal fines for an organizational failure, something that’s becoming more common in regulatory environments like those governed by MiFID II and FINRA. Not only that, think about the personal impact a significant non-compliance incident could potentially have on one’s career. It could go both ways: If you avoid the breach, you saved the day. If you miss it - it’s on you. This underscores the importance of having robust, AI-backed compliance systems that provide a safety net and ensure that no critical issue slips through the cracks.

6. Resource Constraints

Nearly each time we meet with a new company, we hear that compliance teams are under-resourced yet tasked with immense responsibilities. It’s a constant balancing act, trying to do more with less while ensuring adherence to complex and dynamic regulations. We’ve consistently found that teams that adopt scalable AI solutions are better able to manage their workloads. Technology can pore through large databases and stay up to date on changing regulations, freeing up the team to focus on high-impact tasks and business development, rather than getting bogged down in routine checks.

7. Culture of Compliance

Creating a culture of compliance is perhaps one of the most challenging aspects of the compliance officer’s role. I’ve seen organizations where compliance is viewed as a box-ticking exercise, which is a recipe for disaster, particularly when dealing with regulations like MiFID II and Consumer Duty that require a more embedded approach. It’s critical to embed compliance into the organizational culture, and tools that enable continuous monitoring and employee training are invaluable. These tools help shift the perception of compliance from a burden to a shared responsibility.

8. Internal Audits and External Examinations

The pressure of audits, whether internal or external, is a reality that every compliance officer faces. I’ve seen how the fear of uncovering a non-compliance issue can lead to sleepless nights. However, those who utilize automated audit trails and real-time monitoring find themselves better prepared, with less stress during audit periods. This is something I’ve often recommended, as it brings peace of mind knowing that the systems in place are reliable and thorough.

Some case studies of compliance failures point to the serious consequences of inadequate risk management. In 2022, The Financial Reporting Council (FRC) imposed fines totaling £46.5 million on large audit firms for audit failures. Notable cases include the audits of Patisserie Holdings, Stagecoach, Conviviality, Rolls-Royce, and Galliford.

Compliance officers can protect their organizations from audit failures by proactively identifying potential risks early and implementing comprehensive mitigation strategies of both internal and external threats.

The Weight of Responsibility

The role of a compliance officer is undeniably one of the most challenging in the financial industry, even if at times it can be underappreciated. The stakes are high, and the margin for error is razor thin. But with the right tools and a proactive approach, these challenges can be managed effectively. By staying informed, leveraging advanced compliance technology such as Sedric, and promoting a culture of compliance, we can turn these nightmares into opportunities for improvement and success.